In the second quarter of 2024, the outlook for economic development remains restrained, although there are some indications of growth. In Europe, the sentiment is somewhat ambiguous and short- and medium-term forecasts remain cautious. In this issue of DHL Road Freight Market News, we take a closer look at key details and trends for April, May, and June 2024. Where does the EU economy stand after the second quarter of 2024 and how is European road freight developing? Trends for the fourth quarter of 2023 can be found in our previous issue.

Slow Acceleration in Economic Growth in the EU – Downside Risks Remain

The EU economy grew by around 0.3% in the first quarter of 2024, returning to growth after two previous quarters in which GDP fell by 0.1%. Although the first few months of this year have been encouraging, the macroeconomic environment has not changed significantly: Russia’s war in Ukraine continues unabated, the situation in the Middle East remains tense, and geopolitical blockades continue, particularly regarding China and the United States. The outcome of the European elections and their consequences, such as the dissolution of the French parliament, and the uncertainties surrounding the results of the U.S. elections in November also impact global trade and energy markets and thus pose a risk to the economy.

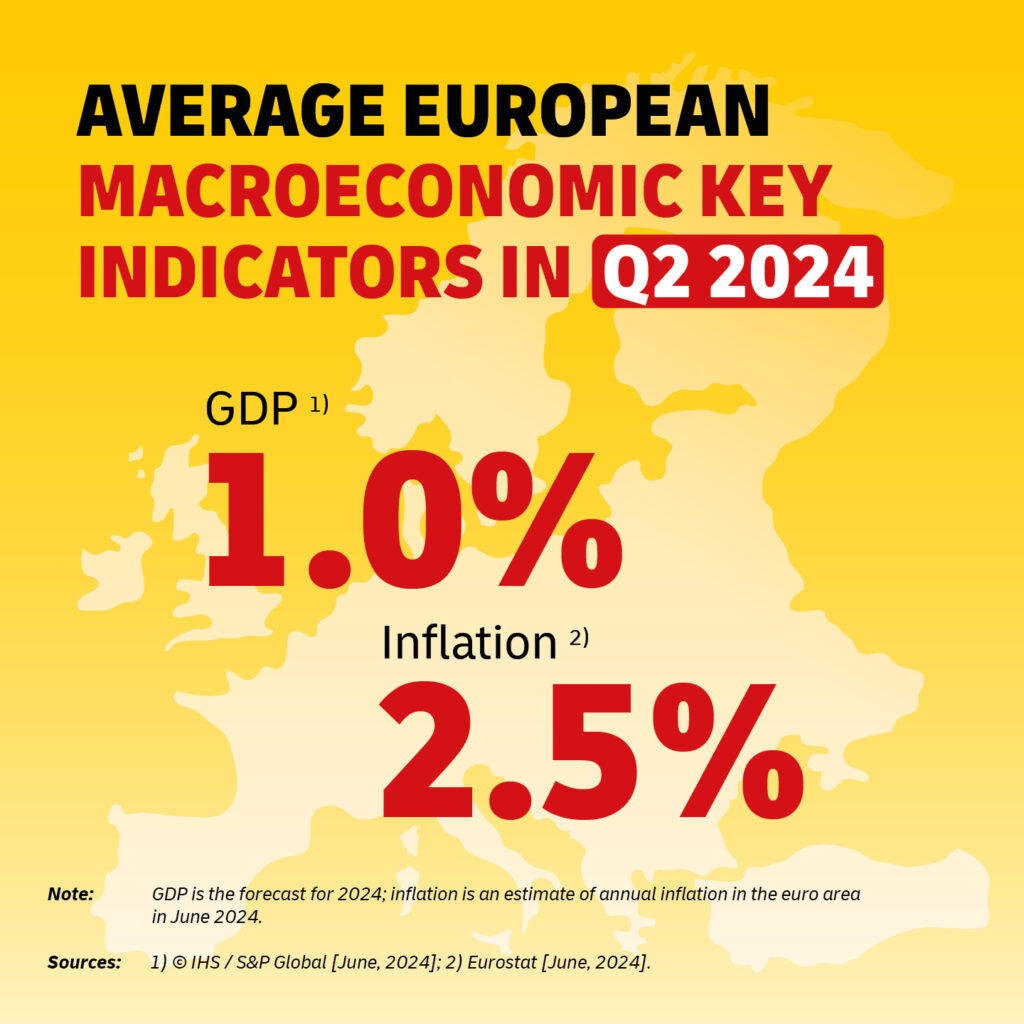

Nevertheless, the EU Commission expects growth to gradually accelerate over the course of this year, forecasting GDP growth of 1.0% in the EU, rising by a further 0.6 percentage points in 2025. Forecasts by other institutions, such as the OECD and the International Monetary Fund (IMF), point to GDP growth of 0.7-0.8% in 2024 and 1.5% in 2025. These forecasts are mainly based on private consumption, as declining inflation should have a positive effect on purchase power.

Eurozone annual inflation is estimated at 2.5% in June, compared to 2.6% in May. The EU Commission expects the rate to drop to 2.1% by 2025. Based on this inflation outlook, the Governing Council of the European Central Bank (ECB) recently decided to reduce its monetary tightening and cut its key interest rate, which had remained unchanged at a high level for nine months. It is currently expected that the rate cut in June will be followed by further rate cuts this year. Falling interest rates, a stable labor market, and continued income growth are likely to provide further momentum to the economy.

This positive outlook led to a corresponding improvement in sentiment in the early months of the second quarter, leaving no doubt about the expected upturn. In May, well-founded sentiment indicators continued to support economic optimism. The S&P Global Purchasing Managers’ Index (PMI), for instance, indicated a clear upturn in the eurozone economy on the back of stronger growth in new orders and employment, rising from 51.7 points in April to 52.3 points in May. This signals not only growth for the third consecutive month, but also acceleration to a level not seen for 12 months. The service sector was the main driver of growth, while industrial production did not grow but fell only slightly.

However, it appears that the recent hopes for growth have been somewhat dampened in June: the PMI fell to 50.8 points in June, suggesting a slowdown in the economic recovery. While the service sector continued to boost growth, industrial production dropped to its lowest level since late 2023, as incoming orders decreased slightly for the first time in four months.

Contrary to expectations in May, the index did not continue its upward trend in June, impairing hopes of a recovery, especially as new orders, generally a good indicator of short-term economic trends, fell sharply.

While this development clouds the outlook for economic recovery to some extent, the PMI continues to signal growth for the fourth consecutive quarter, ultimately suggesting that GDP is likely to increase again in the second quarter of 2024.

Germany Expects Economic Recovery Despite Only Cautious Improvement in Sentiment

In line with this subdued outlook for the EU economy as a whole, the German economy is also weakening. Last quarter, experts estimated that the economy reached the bottom of the trough by the first quarter of 2024 and that moderately positive growth rates could be expected for the rest of the year as consumer spending picked up. After rising by 0.2% quarter-on-quarter in the Q1 of 2024, GDP is expected to grow at a similar rate in Q2, according to the German Federal Bank. Experts expect positive stimuli in particular from private consumers.

In May, the results of the Consumer Climate Indicator by the German market research company GFK supported these assumptions and pointed to a positive trend in consumer behavior, with the index showing an improvement in consumer sentiment for the fourth time in a row. However, the recovery in consumer sentiment in Germany came to a temporary halt in June, with the GfK Consumer Climate Indicator falling from -21.0 to -21.8 points. This is partly due to consumers’ low propensity to buy, which can be attributed to the slightly higher inflation rate of 2.4% in May (compared with 2.2% in April) and the resulting lack of planning security for private households.

The subdued consumer sentiment is matched by a deterioration in business sentiment. The German Chamber of Commerce and Industry (DIHK) reports an overall negative assessment of companies’ business situation. More than half of the companies are particularly concerned about high energy and raw material prices, the continuing shortage of skilled workers, and the persistently high cost of labor. The ifo Business Climate Index also registers a deteriorating sentiment in the German economy in June, with the index falling from 89.3 points to 88.6 points. Similar to the trends in the S&P Global PMI and the GfK Consumer Climate Indicator, the ifo Institute also suggests that the improvement in sentiment is pausing. Especially the declining order backlog in the manufacturing industry and the cloudy mood in the wholesale and retail trade are having a negative impact.

Industry also faces continuing challenges. The order situation is tense, and it is likely to take some time before falling interest rates and a reticent global recovery translate into significant growth in industrial production. Accordingly, the sentiment in the automotive industry, one of Germany’s largest industrial sectors, is bleak, especially when it comes to future business expectations. This is due not only to international competition, with Chinese manufacturers increasingly making their presence felt on the European market, but also to the overall transformation of the automotive industry in terms of digitization, autonomous driving, and electric mobility.

In view of the most recently published indicators, the picture of the German economy at the start of the summer is rather subdued. With an increasing improvement in the general conditions, above all the development of the inflation rate and the associated less tight monetary policy, it can be assumed that there will be supportive impetus on the part of consumers. Strong wage growth and a still robust labor market could stimulate private households to consume more in the near future.

The current trend in inflation is also supportive: the inflation rate in June is estimated at around 2.2%, the same level as in April and slightly lower than in May. The Federal Ministry for Economic Affairs and Climate Action estimates inflation at 2.4% for 2024 as a whole, before dropping to around 1.8% next year, which is below the ECB’s target. In addition to the inflation rate gradually stabilizing at a level of 2%, the turnaround in interest rate policy announced by the ECB will lead to improved financing conditions, thus representing an important milestone.

Experts therefore expect the economic recovery in Germany to continue in the second half of the year, albeit at a slower pace overall. This is because it is likely to take some time before falling interest rates and the tentative upturn in the global economy are reflected in noticeable growth in German industrial production.

As uncertainties remain, current forecasts for German economic growth in 2024 vary accordingly: the EU Commission, for example, believes that Germany as one of the EU’s strongest economies will grow by only 0.1% this year. The Kiel Institute for the World Economy (IfW) and the German Council of Economic Experts predict GDP to grow by 0.2%, while the German government itself estimates that the German economy will grow by 0.3% this year. The ifo Institute is even forecasting economic growth of 0.4%. Some economic experts do not expect a slight acceleration until 2025 and are then forecasting economic growth of around 1%.

Development in the Road Freight Market

Although developments in the road freight sector generally go in step with economic developments, the latest industry surveys paint a more positive picture. For example, the logistics indicator by the German logistics association BVL shows that not only have the business situation and the business climate improved, but business expectations are also significantly less pessimistic than in the previous quarter. Despite this positive picture, the outlook for the road freight sector is still worrying, mainly due to the uncertain development of demand.

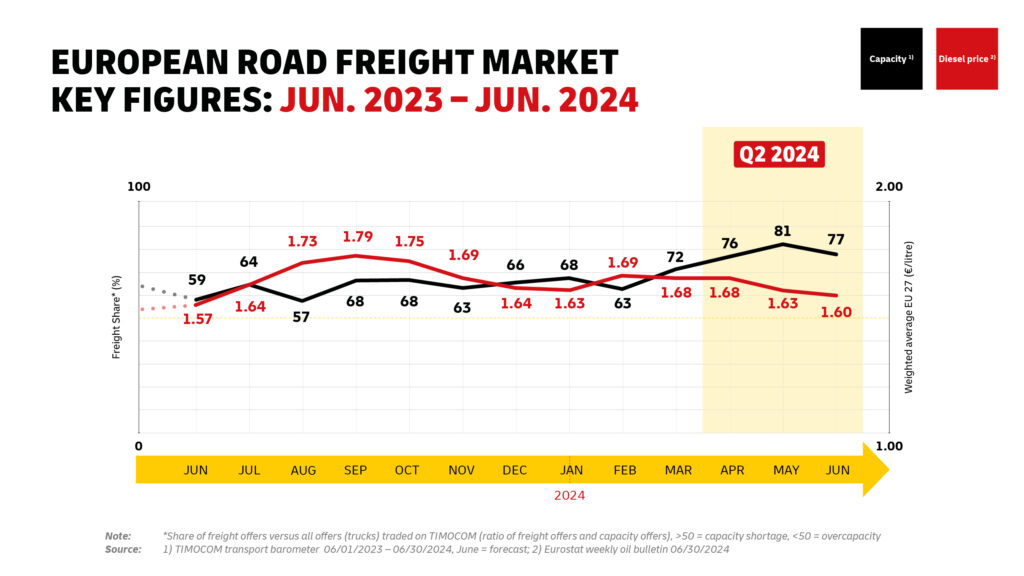

Hence, despite the positive impulses, there is no real trend reversal in the road freight sector. The missing turnaround is also reflected in the development of the capacity index, which is monthly provided by TIMOCOM. It already showed significant capacity bottlenecks in the course of the first quarter, but this was primarily the result of reduced truck fleets. The trend is continuing in Q2 of 2024. In June, the ratio of freight to cargo space was 77:23. According to current forecasts, the ratio will fall to 73:27 in July, which is typical for the summer months.

Freight Rates Stay High

Notwithstanding the difficult market situation, freight rates remain at high levels. Although the price of diesel is moderate at €1.60 per liter for the 27 EU member states, other costs, such as driver costs, continue to rise. Road toll adjustments, such as in Belgium and most recently in Germany, where vehicles with a gross vehicle weight of 3.5 tons or more have been subject to tolls since July 1, are also contributing to rising costs for road freight carriers. In addition, increasing investments in the decarbonization of the road transport sector have to be factored into prices and passed on to clients.

The Market Situation in Summary

Economic development continues to show a complex dynamic with mixed signals from different sectors. The PMI and the Ifo Business Climate Index, two important indicators of the economic situation, both point to ongoing challenges in overcoming economic stagnation. Nevertheless, there are signs of a gradual recovery. Thanks to lower inflation and higher wages, demand is expected to pick up – a development supported by the ECB’s interest rate cuts. As a result, the economy, which has been growing at a below-average rate, is expected to gain momentum.

Outlook for Further Development

Even if the outlook for 2024 and 2025 is cautiously optimistic, existing risks such as the trade dispute with China, uncertainty about the balance of political power in France, and ongoing geopolitical tensions in the Middle East cannot be ignored. These risks could have a negative impact on foreign trade and could also significantly slow the decline in inflation if, for example, energy markets are negatively affected. Irrespective of these risks, the economy is likely to be supported by growth impulses and thus to experience a moderate increase.

The next update, to be published at the beginning of October 2024, will examine market developments in the second quarter of 2024 and the resulting impact on the road freight market. This will ensure continuous open and transparent communication, which is a top priority for DHL Freight.