The generally optimistic mood in the European economic area has so far remained unshaken. In this issue of DHL Road Freight Market News, we look at the key details and trends in the first three months of 2023. Where does the EU economy stand after the first quarter of 2023 and how is European road freight developing? For an overview of what happened in the middle of the quarter, please check out our last issue.

Cautious Optimism for the Overall Economy

Although the global economy continues to be severely impacted by the general economic conditions, a cautiously positive trend is consolidating at the end of the quarter, both among economic experts and among the companies themselves.

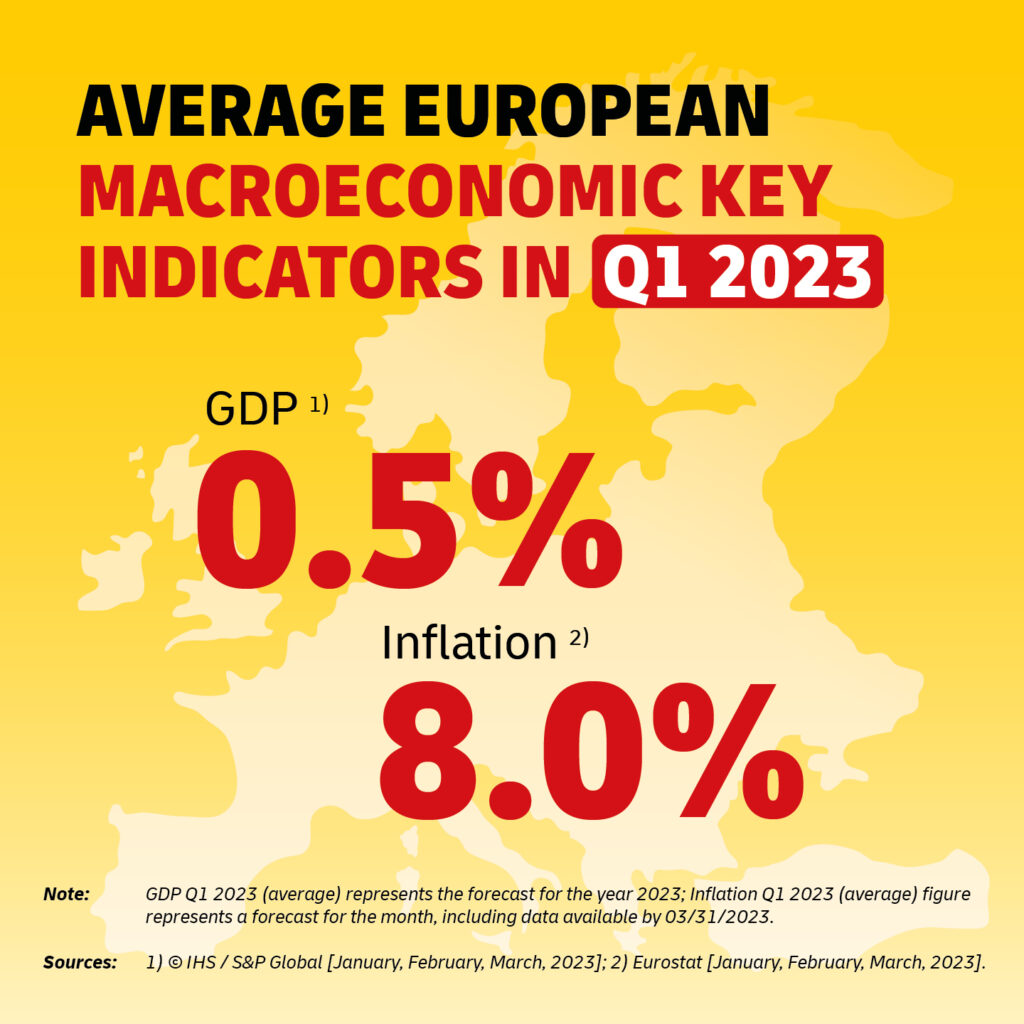

Whereas at the beginning of the year the World Bank was still assuming global growth to be slowing due to the persistently high price level and increased interest rates, individual indicators have been revealing a moderately positive sentiment since the beginning of the year. For example, S&P Global reported an improved forecast for European gross domestic product (GDP) for 2023: in January, a stagnation was still expected for 2023, but the outlook improved to 0.4% growth in February and even to 0.5% in March. A crucial factor in this improvement is the reduction in inflationary pressure, which will be addressed in more detail later in this article. In addition, China’s reopening after several years of isolation due to the pandemic is also sending positive signals within the economy.

On a global scale, hopes of an economic rebound were growing, too. In March, the OECD raised its forecast for global GDP growth for 2023 from 2.2% to 2.6% (and for 2024 from 2.7% to 2.9%). The OECD also expects slight growth for Germany, Europe’s largest economy – however, the forecast of 0.3% is below expectations for other European industrialized countries.

The OECD assumptions for Germany are in line with the assessment of the German Council of Economic Experts and the Kiel Institute for the World Economy (IfW Kiel). They both now expect a slight improvement in the German economy compared with their forecasts from fall 2022: the Council is more conservative and predicts GDP growth of 0.2%, while IfW Kiel even anticipates 0.5% for 2023. The improved outlook in Germany is based on a slight brightening of sentiment among both companies and consumers. Thus, the consumer climate index of the German market researcher GFK continues its recovery since October 2022 also in March, but nevertheless remains in the negative range. The ifo Business Climate Index in March also rose for the fifth time in succession to 93.3 points, up from 91.1 in February.

Despite Cautious Optimism and Falling Inflation, Economic Risks Remain

As mentioned above, the decline in inflationary pressure is the most important factor behind the economic recovery and the improved sentiment of market participants. For the entire EU, inflation rates continue to decrease in March 2023, having fallen since the fall of 2022: according to Eurostat, the expected annual inflation rate in the EU fell from 10% in December 2022 to 8.5% in January 2023, where it remained in February and finally fell to 6.9% in March. This means that the slight decline in the inflation rate has continued since fall 2022 but remains at a high level.

Throughout the first quarter, the highest inflation rates were in the Baltics, as in the previous year (most recently in March at 17.3% in Latvia, 15.6% in Estonia and 15.2% in Lithuania). In Germany, the figure is above the EU average, with an expected annual inflation rate of 7.8% in March 2023. Admittedly, it must be noted that for the March values, the comparative data from March of the previous year – after the outbreak of the Ukraine war – were already significantly higher. This base effect distorts the view of price developments.

In the long term, hope remains that inflation could fall even more sharply. Rising interest rates, reduced bottlenecks in supply chains and falling energy prices could bring inflation down significantly to 3.1% in 2024, according to the OECD.

Notwithstanding these developments, the economy continues to face major challenges:

Not only the constant uncertainty due to the unpredictable course of the Ukraine war or other geopolitical tensions, for example between the US and China, are a cause for concern. The increase in the key interest rate by the European Central Bank (ECB) to 3.5% in March also contributed to this. This is because high key interest rates can become a burden on the economy if the order situation in industry develops critically and a downturn in industry also affects other sectors of the economy after some time.

Other indicators show how tense the climate in industry remains despite improved forecasts. For example, after a slight recovery in February to 48.5 points, the S&P Global Manufacturing PMI now shows a slight decline in March to 47.3 points. The European Commission’s Economic Sentiment Indicator (ESI), which assesses the general mood of businesses and customers in the EU, also recorded a slight decline in March after rising slightly at the beginning of the year.

The turbulence in the banking industry, most recently the takeover of Credit Suisse by UBS, is likewise not boosting optimism about further economic development this year. A global financial crisis of the kind caused by the collapse of Lehman Brothers in 2008 seems unlikely at present, but against the backdrop of financial turmoil combined with possible further increases in key interest rates, the moderate rise in European economic output since the beginning of the year remains somewhat fragile.

Development in the Road Freight Market

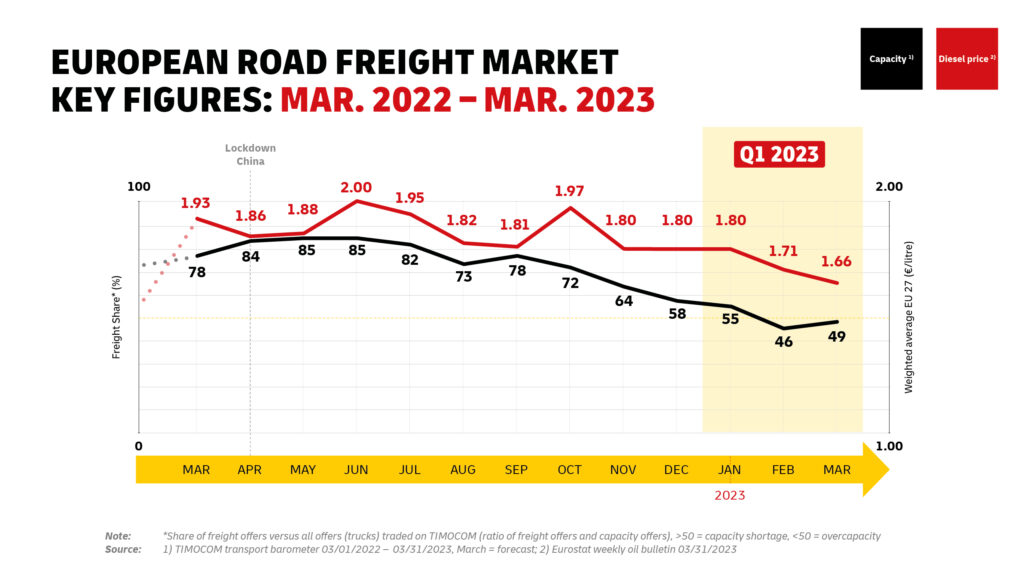

The easing in the capacity bottleneck situation, which was already evident in Q4 2022, continued in Q1 2023. After an excess capacity was recorded for the first time in February 2023 (46:54), the TIMOCOM Transport Barometer recorded a slight decline in available freight capacity again in March with a ratio of 49% freight share to 51% available cargo space. This development is most likely due to the seasonal nature of the road transport market, as the weeks around Easter are usually characterized by an increase in volumes.

This is also the reason for TIMOCOM’s current forecast, which points to a capacity bottleneck – albeit a minor one – in April.

Price Level of Freight Rates Declining Only Slowly

A glance at the factors relevant to freight rates shows there was not only a higher supply of spare capacity in the first quarter of 2023 than in previous quarters, but also a further drop in diesel prices. While the weighted average diesel price for the 27 EU member states was still at 1.80 euros/liter until January, it is now declining and was at 1.66 euros/liter in calendar week 13, according to Eurostat.

At the end of Q1, however, these developments have not yet been reflected to any great extent in freight prices for land transportation, as freight prices in general have fallen only slightly since the beginning of the year. Nevertheless, a clear trend can be seen in spot prices: after very high rates throughout last year, available capacity is now having an impact on the market, leading to increased competition between freight forwarders and, as a result, significant reductions in spot rates.

At present, it is quite difficult to predict the future development of the price level in concrete terms. If sufficient capacity will continue to be available on the market, freight prices may decrease. But it is also imaginable that freight prices will remain high, in particular due to toll increases in various European countries and rising wage costs.

The Market Situation in Summary

At the end of the quarter, economic growth in the euro area is expected to improve in 2023, albeit only slightly. Sure enough, the outlook is clouded by the current market environment, which remains volatile due to ongoing and new risks – such as the recent turmoil in the banking industry.

In European road freight, the current capacity development reflects the positive but nonetheless subdued economic development. Apart from spot prices, freight prices seem to have been falling only slowly since the beginning of the year.

Outlook for Further Development

The uncertain economic situation in times of crisis makes any reliable prognosis for the coming months impossible. In particular, the outlook for the European road freight market depends on various unforeseeable factors. But after the mostly positive trends of the first quarter, there is reason to hope the economic upturn will continue.

Compared with the previous year, however, when events were in overdrive, the pace of new incidents has now slowed considerably. For this reason, we will only report on a quarterly basis on the most important changes, facts, and trends in the future. The next update will be released at the beginning of July and will once again provide an overview of economic affairs and the associated implications for the road freight market. You can rest assured we will maintain our commitment to open and transparent communication – because that is DHL Freight’s top priority.