February 2023 has brought a restrained optimism towards the economic development in the euro area. In the February/March issue of DHL Road Freight Market News, we take a closer look at the EU economy in the middle of the first quarter of 2023, with a special focus on the situation of European road freight. Information on trends at the beginning of the year can be found in our last issue.

Euro Economy: The Mood Brightens in February

March 1 marks the start of meteorological spring and brings with it a gratifying recognition: the feared gas shortage failed to materialize in winter 22/23. Moreover, with problems in the global supply chain easing in many sectors and, at the same time, price pressure in the euro zone decreasing, both European companies and financial market experts in February are much more optimistic about the EU economy than they were just a few months ago.

Eurostat, the statistical office of the European Union, provides the figures. According to first projections, the annual inflation rate in the euro zone has fallen again, albeit only slightly: from 8.6 percent in January to 8.5 percent in February. The highest inflation rates continue to be registered in the Baltic states (Latvia: 20.1 percent; Estonia: 17.8 percent; Lithuania: 17.2 percent). In Germany, Europe’s largest economy, the figures are above the EU average, too, with an expected annual inflation rate of 9.3 percent.

Rising Consumer Confidence in Economic Activity in the Euro Area

The decline in inflation has continued slowly but steadily since November 2022. This obviously brings some relief for European consumers, whose spending mood is recovering slightly. Despite the persistently high price pressure, consumer sentiment in February was again better than in the previous month.

This is evident, for instance, from the EU Commission’s consumer confidence index, which reflects private households’ expectations for economic development in the euro zone and thus constitutes an early indicator for consumer activity. The index recently rose by 1.5 points to -20.6 points, the fifth monthly increase in succession. However, it is still a substantial step away from its long-term average of 10.06 points for the period 1985-2023.

This cautious optimism on the consumer side is being echoed by other economic indicators. These include, among others, the economic barometer of the Centre for European Economic Research (ZEW) and the Ifo Business Climate Index. The financial market experts surveyed by ZEW not only have a positive view of the current situation in Europe but are also increasingly confident about future economic developments. This also applies to Germany. For the first time since February 2022, the German economic situation for the next six months is considered to be noticeably better. This assessment is reflected in the development of the ifo Institute’s business climate index in February, which has risen once again compared with January, indicating a more positive assessment of the business situation.

All in all, it can be stated that the European economy is more resilient than economists had originally expected. In February, S&P Global no longer predicted stagnation for 2023, but a slight increase in European GDP of 0.4 percent. This optimistic forecast is also shared by the EU Commission, with Brussels being even more confident: the Commission’s growth forecast for 2023 has recently been raised from 0.3 percent to 0.9 percent.

No Recession, Tight Fiscal Policy, and Development of Industry

The European Central Bank (ECB) concurs with this optimism, indicating that growth within the euro economy could develop much more positively than assumed in the last ECB projection (0.5%). Despite the assumption that a recession in the euro area most likely will be avoided, it is anticipated that the ECB, due to the persistently high price level, will stick to its current course in the fight against inflation. Should the next ECB interest rate meeting in mid-March result in the generally expected increase of 0.5 percentage points, this would be the sixth increase since the exit from the zero interest rate policy in July 2022.

A number of experts are sceptical about the forthcoming interest rate increase by the ECB. Some analysts fear that higher key interest rates could put the brakes on the economy. They suggest treating the current economic upturn with caution. The basic assumption is that interest rate measures usually have a delayed dampening effect on the economy and that the full impact of the current measures may thus not be felt for several months.

Despite the brightening of the mood in the euro zone concerning the economic development and the basically positive climate among consumers, the euro industry continues to face major challenges. S&P Global, for example, indicates that there may be a prolonged stagnation in orders. This may be compensated for in the short term by serving accumulated orders from the pandemic period, but in the long term it could have a significant impact. With further interest rate increases, the order situation in industry is likely to worsen and after a certain time lag, a downturn in industry would also make itself felt in the other sectors of the economy. In this respect, it remains to be seen how order intake will develop in the coming months.

Development in the Road Freight Market

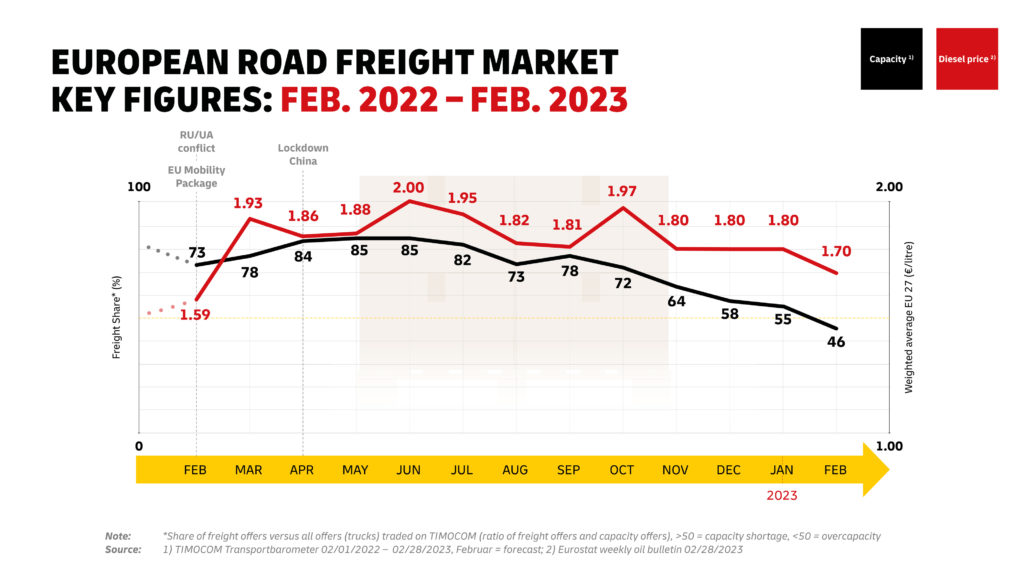

As previously reported, the capacity bottleneck has relaxed significantly since the end of 2022. After TIMOCOM’s transport barometer reported a value of 55:45 for the ratio of freight to available cargo space in January, the proportion of available cargo space increased significantly in February. As a result, freight demand of 46 percent contrasted with 54 percent of available cargo space.

Compared to the tight capacity bottleneck situation last year, especially in comparison to February 2022, when the demand/supply ratio was 73:27, there is now a clear relief on the European freight market in terms of available capacity: February 2023 is the first month since July 2020 in which there is a surplus of capacity available on the market.

Overcapacities and Lower Diesel Prices Are Not Reflected in Freight Rates – Price Level Remains High

While the capacity bottleneck in the market has improved significantly, road freight rates remain largely unaffected and at a high level. Even falling diesel prices have not yet led to a significant drop in freight rates. While the diesel price for the 27 European member states recently stagnated at 1.80 euros/liter, it fell in February and now amounts to 1.71 euros/liter in the ninth calendar week, according to Eurostat.

The current easing in diesel prices is offset by toll increases in various European countries and rising wage costs, which will probably be further fueled by the shortage of truck drivers in the transport sector. These factors are relevant to freight prices and their development suggests that rates will remain high in the future.

The Market Situation in Summary

Due to the slight decline in inflationary pressure and the robust economic performance to date, the cautious optimism of economists and market participants continues. Contrary to the stagnation that was originally predicted, slight economic growth is currently expected in the euro area in 2023. However, this forecast is subject to considerable uncertainty, as the overall market environment remains volatile and geopolitical developments cannot be foreseen.

Considering the road freight market, we see that demand for cargo capacity is lower than the supply of cargo space: for the first time in almost three years, there is overcapacity in the European road freight market. What is yet to be seen is how the relationship between supply and demand will develop, especially in view of the Easter period.

Outlook for Further Development

Given the uncertain economic situation in times of crisis, reliable forecasts continue to be difficult to provide. This especially applies to the European road freight market, whose development depends on various factors. In our next update, which will be published at the beginning of April, we will reconsider general market trends and their associated implications for the road freight sector. This is how we want to ensure that you are always at the cutting edge. After all, transparent communication is a top priority for DHL Freight.