The euro economy has made a subdued start to 2023 despite the recent upturn at the end of 2022. In our January and February issue of DHL Road Freight Market News, we recap the general economic development at the beginning of the new year and the situation of European road freight in particular. Information on trends in November and December 2022 can be found in our last issue.

Looking Back at the European Economy in 2022: Record Inflation, but No Recession

A post-pandemic recovery and thus a flourishing economy was commonly expected for 2022. These expectations were countered above all by the Russian war of aggression against Ukraine and the ensuing impact on the European energy market. Great expectations were followed by even greater concern in many EU countries. By the fall of 2022 at the latest, the economic alarm signals could hardly be ignored. A comprehensive energy crisis was feared due to restricted supply options with far-reaching consequences for industry and the economy. Economists warned of a massive economic downturn in all major European economies, especially Germany.

These consequences were reflected notably in high price levels, as inflation in the EU rose month by month until it reached a record 10.6 percent in October. To counteract this trend, political measures were taken throughout Europe, for example to safeguard energy supplies. Price caps or support packages were able to mitigate the negative impact of the massive rise in energy costs on companies and private consumers.

The European Central Bank (ECB) also responded to the persistently high inflation and raised the key interest rate no less than four times – to 2.5 percent by the end of 2022 – in order to curb inflation in the euro area. Since November, effects of the respective measures have been noticeable. According to Eurostat, the statistical office of the European Union, the annual inflation rate in the EU was lower in December, but still stood at 9.2 percent. In the draft of its annual economic report, the German government already indicated that the inflation trend had probably passed its peak, which has since been confirmed in January.

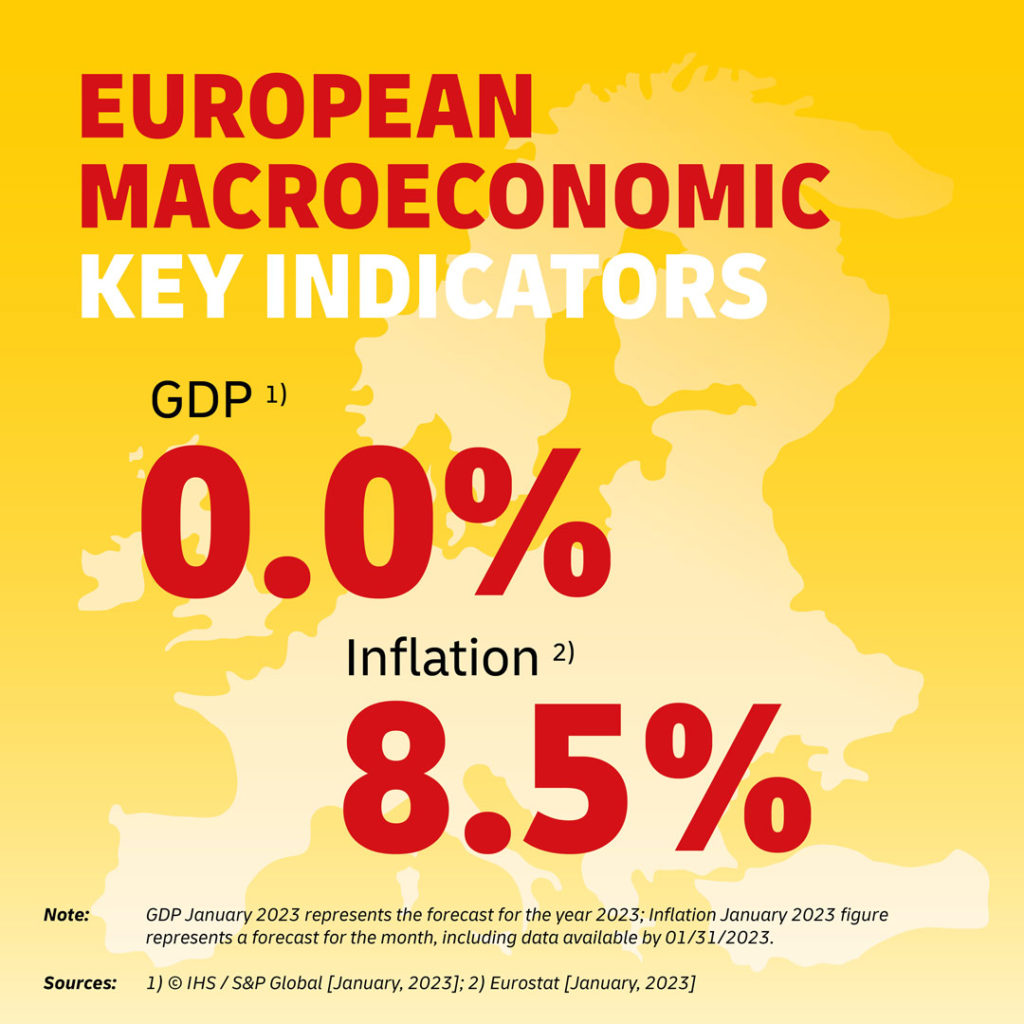

Notwithstanding the challenges facing the European economy in 2022, economic development proved to be much more robust than initially feared by experts: S&P Global indicated a value of 3.4 percent for European GDP (excluding Russia) at the end of 2022.

What Does the Future Hold for 2023?

It is clear after the volatile year 2022 that forecasts for 2023 can only be made with reservations. However, it is undisputed among economic experts that the global economy will continue to be under severe pressure in 2023. The latest World Bank report, for example, predicts that global growth could slow down due to persistently high price levels and higher interest rates.

Contrary to this expectation, though, there are currently signs of cautious optimism in Europe regarding the economic development. This is reflected, for instance, in the S&P Global Purchasing Managers’ Index, which reveals that the general mood in the industry improved slightly at the beginning of the year. This brighter outlook is also confirmed by the ifo Business Climate Index for the German economy – expectations are noticeably less pessimistic than recently in 2022.

This is mainly due to promising economic signs of lower inflationary pressures, fewer bottlenecks in supply chains, and the fact that gas shortages could be avoided so far. The easing on the energy market is also apparent in the inflation rate: according to Eurostat, the annual inflation rate in the euro area fell from 9.2 percent in December 2022 to 8.5 percent in January 2023. As in previous months, the highest rates were again recorded in the Baltic states (Latvia: 21.6 percent; Estonia: 18.8 percent; Lithuania 18.4 percent).

Despite the now slightly falling price level, the ECB is continuing its fight against high inflation in the euro zone and is raising the key interest rate again in January by 0.5 percentage points to 3.0 percent.

In theory, tight monetary policy increases the risk for the economy to be slowed down by declining consumption. In 2022, the euro area economy was actually more robust than expected, thanks in particular to private consumption, which had risen enormously in early 2022 after the COVID-19 years. Meanwhile, rising prices are impacting private consumption as well. In view of the significant drop in real disposable incomes, it is currently unlikely that consumption will increase significantly in 2023. Consequently, according to data from S&P Global, growth in the European economy of 3.4 percent in 2022 could be followed by a slight contraction or stagnation in European gross domestic product. Growth of 0.0 percent is expected for 2023.

Road Freight Market – Trends and Expectations

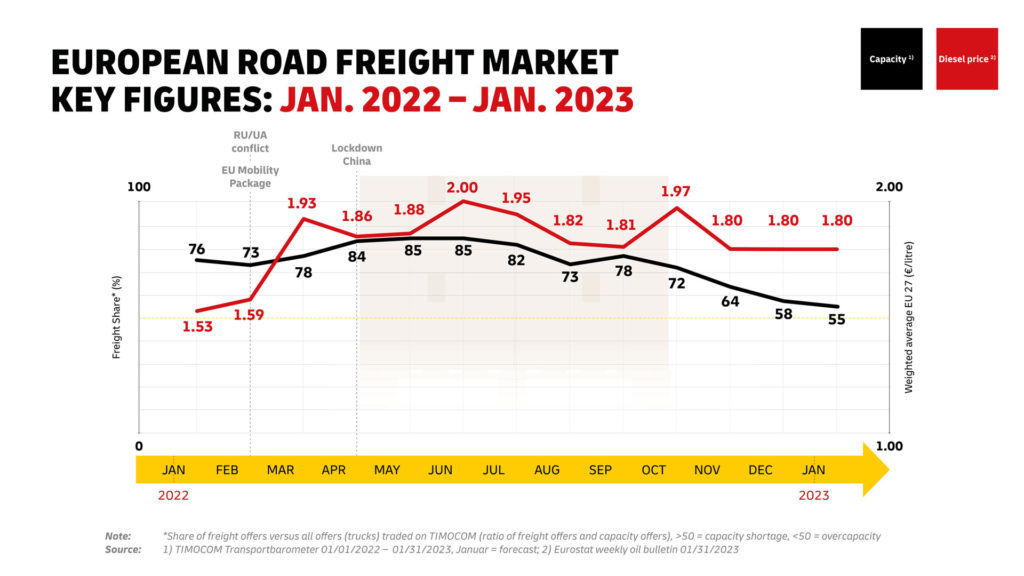

After the demand for freight volumes in the European road freight market had almost permanently exceeded available freight capacity in 2022, the capacity bottleneck eased significantly by the end of 2022. In December, TIMOCOM noted a sharp decline in freight demand relative to the availability of cargo space and a Europe-wide decline in freight offers.

Accordingly, TIMOCOM recorded a ratio of 58 percent freight to 42 percent available cargo space in December. In previous months, cargo space utilization was at times only 15 to 20 percent. The December trend, and thus the reduction in capacity shortages, continued in January, with a 55:45 ratio of freight to available cargo space reported at the beginning of the year.

Turnaround for European Road Freight: Capacity Bottlenecks Dissolve, Road Freight Price Index Stays High

The fourth quarter of 2022 could prove to be a turning point given the development of supply and demand for freight and cargo space in the European transport market. Surely, a seasonal peak followed by a slump in freight supply is by no means unusual. However, compared to seasonal trends in previous years, a much faster decline in freight supply can be observed at the end of 2022 – the slump typically occurs not before January.

One possible explanation for this development is the volatile development of the past year with its numerous challenges for road freight – including capacity and supply bottlenecks. This has led to many companies securing transport capacity early in order to have sufficient freight capacity available during their peak season. This has taken the usual momentum out of freight volumes in the run-up to Christmas.

In addition, there is the shortage of drivers: the persistent lack of personnel is forcing some transport companies to turn down orders and reduce cargo space, even though there are enough resources in their fleets. Moreover, the easing of capacity bottlenecks also indicates the fundamental economic development and the related decline in market volume. This is illustrated, for example, by the German truck toll mileage index, which correlates directly with economic activity. It states that in December 2022 there were 4.9 percent fewer trucks on the autobahns than a year earlier. At the same time, providers in the road freight sector report significant volume declines that will continue at least until the second half of 2023.

Further road freight statistics reveal that, although the situation in terms of lacking capacity on the road freight market has improved, this is still not reflected in freight rates. Even the now somewhat weakened diesel price, which for the 27 European member states in the fourth calendar week of 2023 is a weighted average of 1.80 euros per liter, is not having a downward effect on freight rates. The road toll increases introduced in 2023 in some countries, including Germany, and rising wage costs are likely to push freight rates up even further, or at least keep them at a high level.

The Market Situation in Summary

The euro economy is starting the new year with hesitant optimism. Even though the fear of a gas shortage has failed to materialize, inflation is leveling off, supply chains are stabilizing, and the economy is proving to be more resilient than expected, the challenges remain considerable and the prospects for economic growth thus bleak. In all European countries, economic stagnation or even a moderate contraction is still not ruled out.

This constant risk remains, as the gas supply situation could potentially tighten depending on the severity of the winter month ahead and supply chains could again be affected by bottlenecks due to a high COVID infection rate in China. Finally, geopolitical disputes, as, first and foremost, the war in Ukraine, could put further pressure on international trade.

European road freight is currently experiencing a relaxation in terms of available capacity, but not in terms of freight rates. The next peak season will probably show to what extent this shift from capacity bottlenecks to a more balanced ratio of freight demand and supply corresponds to a long-term turnaround or whether it is merely a snapshot. From experience, there is an increase in freight offers before Easter.

Outlook for Further Development

Given numerous political and economic imponderables, forecasts for this year remain somewhat unreliable. The general conditions can change at any moment. Especially in such times, open and transparent communication is a top priority for DHL Freight. The next update with details on the course of the still young business year 2023 and the road freight market will therefore be published at the beginning of March.