The dampened mood of the second quarter continues. Although slight annual growth is expected for the European economic area in the third quarter, the situation remains tense, particularly in Germany. In this issue of DHL Road Freight Market News, we will take a closer look at the key details and trends in July, August, and September 2023. How will the EU economy perform after the third quarter of 2023, and how is European road freight expected to develop? Information on the trends in Q2 of 2023, you can find in our last issue.

Weak Economic Growth in Europe – and Subdued Prospects for the Coming Year

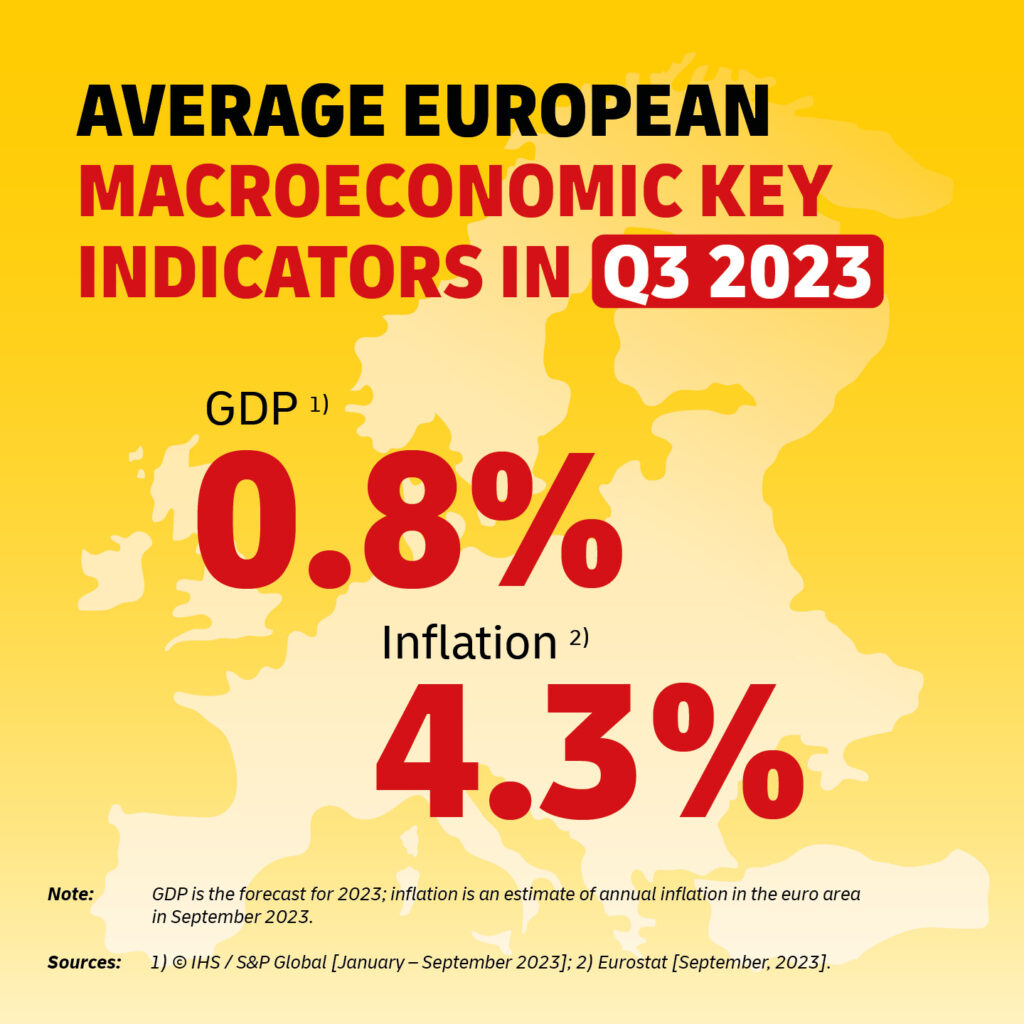

Whereas forecasts in the previous quarter still assumed very weak global economic growth, with estimates ranging between 2.1% and 2.5%, the predictions for the third quarter of 2023 are significantly better. The International Monetary Fund, for example, has raised its outlook for this year. The estimated global growth of 3.0% is lower than the previous year’s figure (3.5%), but higher than predicted in April. However, economic growth remains weak by historical standards, which is also reflected in Europe.

In its latest summer prognosis, the European Commission takes a much more skeptical view of the economy in the euro zone than it did in spring. Most recently, the Commission lowered its growth prediction for the EU economy in 2023 from 1.1% to 0.8%. S&P Global‘s September forecast also assumes economic growth of 0.8%. Despite easing inflation, a robust labor market, and recovering real incomes, the weaker growth momentum in the EU is likely to continue – mainly due to the effects of restrictive monetary policy, which will continue to hold back economic activity. This is also reflected in the forecast of the European Commission, which lowered its growth prediction for 2024 from 1.6% to 1.3% at the beginning of September.

Well-founded indices such as the Eurozone Manufacturing PMI, which at 43.4 points in September remains well below the growth-indicating mark of 50.0 points, also confirm that there is no sign of relief in the near future. At 43.4 points, a decrease of 0.1 points compared to August, the PMI index points to a continuing downward trend in the industrial sector.

Bleak Prospects for Germany

The German expert consortium “Projektgruppe Gemeinschaftsdiagnose”, comprising leading economic research institutes such as the German Institute for Economic Research (DIW), the ifo institute, and the Kiel Institute for the World Economy (IfW Kiel), is predicting a 0.6% decline in Germany’s gross domestic product for 2023. This represents a downward revision of 0.9 percentage points on the forecast made in spring 2023 (0.3%). The bleak outlook for the German economy this year is also underlined by the DIW economic barometer. In August, the barometer stood at 90.3 points, the same as in July. Since May, the barometer has thus been well below the neutral 100-point mark, which indicates average growth.

The ifo Business Climate index for Germany confirms that the national business climate is at a historical low. The index fell to 85.7 points in September, from 85.8 points in August and 87.4 points in July. The reason for the depressed economic mood in Germany is the current industrial weakness. As the International Monetary Fund explains, this is a result of high energy prices. The country is also experiencing the effects of comparatively weak global trade. Germany, whose economic model has for many years been based on the export of high-value products such as cars, has suffered particularly from the global slowdown in demand.

However, there is a glimmer of hope for the coming year. According to the experts of the “Projektgruppe Gemeinschaftsdiagnose”, the German economy could regain momentum in 2024 with an expected growth of 1.3% over the year. Less optimistic is the outlook of the Macroeconomic Policy Institute (IMK), which forecasts growth of only 0.7% for Germany in 2024 due to high interest rates and a subdued global economy – as does the Association of German Banks (BdB), which even expects growth of only 0.3%.

Inflationary Pressure on the Decline – Still Energy Costs Pose a Risk

Inflationary pressure in the euro zone continues to ease gradually: While Eurostat reported an annual inflation rate of still 5.3% in July, the rate is estimated at 4.3% in September. Germany, with 4.5% in September, also recorded a significant decline of 1.6% compared with the previous month. This is the lowest value since the outbreak of war in Ukraine. The last time that the inflation rate was lower than in the current month was in February 2022 (+4.3%). To further counter inflationary pressure, the European Central Bank is sticking to its measures and recently raised the key interest rate for the tenth time in succession. It now stands at 4.5% – with further increases possible.

In line with the persistently high inflation rate, the private propensity to consume in Germany has been remaining at a low level for more than a year. The last time it was as low and even below the current value was during the severe financial and economic crisis in 2008. Correspondingly, a study by the GfK, a Germany-based consumer research company, indicates a consumer climate of -25.6 points in September and expects a further decline of 0.9 points in October. Nevertheless, leading research institutes expect consumption to recover, once the inflation rate normalizes. This may already happen next year, when inflation in Germany is expected to fall significantly to a rate of just 2.6%. Thus, private consumption could soon boost the economy again if consumers’ purchasing power grows due to the easing of price pressure and perceptible wage increases.

Development in the Road Freight Market

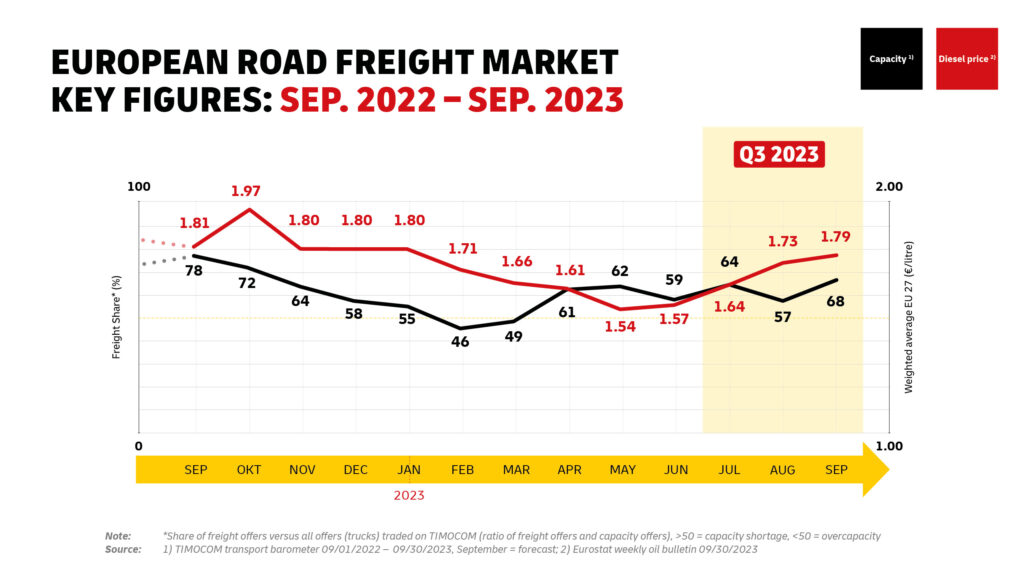

After the year had begun with an excess capacity, a decline was recorded during the second quarter which continued at the start of the year’s second half. While July saw a ratio of freight to available cargo space of 64 to 36, August witnessed a typical seasonal decline in volumes and thus a slight easing of available capacity, with a ratio of just 57 to 43. According to TIMOCOM‘s transport barometer, there is once again an increasing shortage of available capacity in September (68:32).

Overall, the development of the capacity index until 2023 and the comparison with the pre-pandemic years indicate that the ratio of freight to available cargo space is in line with the industry trend. After two exceptional years, the market gradually returns to normal.

Renewed Increase in Diesel Prices – Freight Rates Remain at a High Level

In the first half of this year, the price of diesel fell continuously for several months. Since June, however, Eurostat has reported an increase again: From a weighted average of 1.57 euros per liter for the 27 European member states, the price climbed to 1.64 euros in July and is currently at 1.79 euros per liter. This means that prices remain at a high level. One of the reasons for this is the oil price, which is currently on the rise due to high demand and tight supply.

Correspondingly, general freight rates for land transportation remain persistently high. In addition to high diesel prices, increased wage costs for drivers also contribute to rising transport prices. Necessary investments to decarbonize road freight and, not least, the increase in road tolls in many European countries will lead to transport service providers having to raise prices further in the short term.

The Market Situation in Summary

The economic situation in Europe remains tense. Leading research institutes expect only weak economic growth this year and next as well. In some countries, such as Germany, the economy is even expected to shrink, at least this year. At the same time, central banks are trying to push back on inflation with rising interest rates, which is having an impact on investment confidence.

The persistently dampened market situation is reflected in the European road freight market. Capacities are returning to normal and there are significantly more capacities than in the pandemic years. Nevertheless, freight rates remain at a high level. And this will not change for the time being given rising diesel prices, increased toll rates, and necessary investments in sustainable technologies.

Outlook for Further Development

In view of current economic trends and ongoing geopolitical tensions, no change toward a positive economic situation is expected in the short to medium term. Economic development will remain at a low level, also impacting road freight.

The next update, to be published in early January 2024, will focus on the economic events of the fourth quarter and the resulting impact on the road freight market. This will ensure continuous open and transparent communication, which is a top priority for DHL Freight.