The third quarter of 2024 brings no turnaround and economic development remains reserved. This has an impact on the business climate in Europe and Germany: The prevailing mood, as indicated by short- and medium-term forecasts, is subdued. In this issue of DHL Road Freight Market News, we look at the relevant details and trends for July, August, and September 2024.

Where does the EU economy stand after the third quarter of 2024 and how is the European road freight market performing? Trends for the second quarter of 2023 can be found in our previous issue.

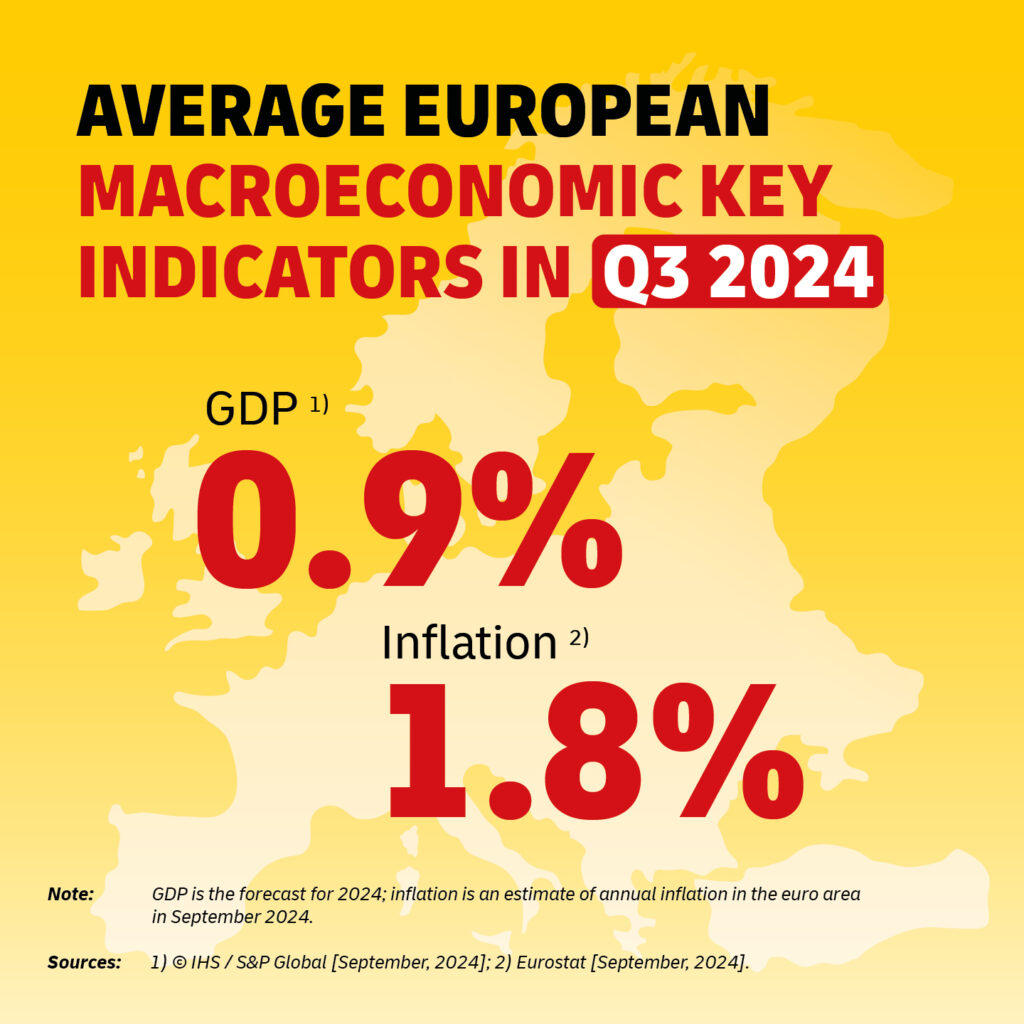

Modest Growth and Falling Inflation in Europe

The European economy remained on a very moderate path of growth in the second quarter of 2024. As for the first quarter, Eurostat initially forecast an increase in gross domestic product (GDP) of 0.3% in the EU and the euro zone, only to lower this figure to 0.9% in September.

There has been little change in the macroeconomic environment over the course of the third quarter: The crisis in the Middle East continues to spread and threatens to involve more and more players, while the Russian war of aggression in Ukraine continues unabated. In addition, the uncertain outcome of the U.S. presidential election brings with it a great deal of uncertainty, and global trade is under pressure from massive increases in energy prices. As a result of these cyclical risks, the economic situation in Europe remains tense.

In response, the European Central Bank (ECB) now assumes that real GDP growth rates will fall to lower levels in the second half of 2024 than those expected in its June projections. The ECB now forecasts real GDP growth in Europe of 0.8% in 2024 and 1.3% in 2025. This is largely in line with S&P Global’s estimate of around 0.9% for 2024. By contrast, the OECD is more pessimistic, forecasting GDP growth of just 0.7% for the euro zone in 2024 in its September interim report, leaving the EU at the bottom of the global growth table. This is unlikely to change much in 2025, although the OECD expects growth of 1.3%. However, this represents a decline of 0.2% compared to the May 2024 estimate.

Business Climate Deteriorates, Consumer Confidence Declines

This development is linked to a cooling of the business climate in the third quarter of 2024. Initially, the Economic Sentiment Indicator (ESI) improved by 0.6 to 96.6 in August, confirming the positive trend that has persisted since September 2023. A closer look shows that this increase was due to an improvement in confidence in industry, trade, and services, while the confidence of consumers and the construction sector declined slightly. However, in September, with the overall ESI remaining stable, confidence in the industry fell by 0.8 points as managers’ assessment of order books became weaker.

The flash Purchasing Managers’ Index (PMI) from S&P Global confirms this assessment by showing a decline in new orders. Overall, the PMI fell from 51.0 to 48.9 points in September and is therefore back below the reference line of 50, signaling a decline in economic output, albeit a slight one in this case. Nonetheless, according to the PMI, the private sector in the euro zone contracted in September for the first time in seven months.

Industry was the main culprit: European industrial production fell for the 18th month in a row in September, and also showed the sharpest decline since the beginning of the year. But the PMI also reflected a slowdown in the services sector: in September, service providers recorded the weakest growth since February 2024. The ongoing economic weakness in the euro zone might have long-term consequences for Europe as a business location and for European competitiveness. The European Commission has asked former ECB President Mario Draghi to provide an expert opinion on how to safeguard Europe’s competitiveness. In his report presented in September, Draghi notes that the EU economy is lagging significantly behind the US and China in terms of growth. Much of this gap is due to lower productivity, particularly in the technology sector. To free Europe from its current static industrial structure and to be able to compete globally with the US and China, substantial investments of 750 to 800 billion euros per year and greater innovative strength are required.

Inflation and Interest Rates

Nevertheless, there is a glimmer of hope: The falling inflation rate could lead to a revival in industrial production and thus have a stabilizing effect on overall economic development. In August 2024, the annual inflation rate in the euro zone was 2.2% (compared to 2.6% in July). This marks a massive decline from 5.2% in August 2023. In September 2024, annual inflation in the euro zone is estimated at 1.8%. While energy prices fell particularly sharply, services continued to become more expensive.

The ECB has responded to slowing inflation in the euro zone by cutting interest rates further, making it cheaper for companies and individuals to obtain credit and thus more attractive to invest. However, as experts believe that the rate cut has already been priced into the markets, it is uncertain whether it will actually trigger an economic stimulus. The ECB expects headline inflation to pick up slightly in the last quarter of 2024, following a decline in September, mainly due to base effects in energy prices. Nonetheless, the inflation target of 2% should be reached.

German Business Climate Clouded by Stagnant Economy

While there was still a slight economic upturn at the beginning of 2024, GDP in Germany fell by 0.1% in the second quarter of 2024. This means that the recovery of the German economy was not only weaker than generally expected at the beginning of the year, but did not take place at all. This trend continued into the third quarter. The German economy is still in a stagnation phase.

Economic Forecasts for Germany Downgraded

Current sentiment and leading indicators do not point to a near-term economic recovery, so economic output will remain at current levels in the third quarter and stagnation will continue through the end of the year. The OECD’s September 2024 interim report predicts real GDP growth of just 0.1% for Germany in the full year 2024, placing it third from the bottom in the world, ahead of Argentina and Japan. Growth of just 1.0% is forecast for 2025, the lowest of the G20 countries.

Other leading research institutes also lowered their economic forecasts for Germany at the end of September. The ifo Institute expects GDP to contract by 0.1% in 2024 and grow by only 0.8% in 2025. The ifo Institute has thus significantly lowered its economic outlook from the summer of 2024 by 0.4 percentage points for 2024 and by 0.6 percentage points for 2025.

As a result, the German economy will be in recession for the second year in a row in 2024. The institutes – namely the German Institute for Economic Research (DIW Berlin), the Ifo, the Leibniz Institutes for Economic Research (RWI Essen and IWH Halle) and the Kiel Institute for the World Economy (IfW Kiel) – doubt that the measures adopted by the German government in the third quarter to boost the economy will be effective in the short to medium term.

The fall in growth expectations in September and the resulting deterioration in the business climate in Germany are also reflected in the decline in the S&P Global HCOB PMI and in the ESI. The HCOB PMI fell for the fourth time in a row in September and, at 40.6, is even more clearly below the 50.0 mark than in August (42.4): the lowest level in the last twelve months. The main reason for this was the even stronger drop in incoming orders, which was the most significant since October 2023. The slowdown in foreign business and falling demand due to ongoing market uncertainties as well as the sluggish automotive industry also contributed to the negative development.

Automotive and Other Industrial Sectors Generate Less Demand

As the most important industrial sector in Germany, the automotive industry has an impact on the entire economy. Decreasing demand has driven the German automotive industry deeper and deeper into crisis in 2024. Accordingly, the business climate in the German automotive industry has worsened significantly. The ifo Business Climate Index for the automotive industry fell by 6.2 points to -24.7 points in August.

However, the demand situation is critical not only in the automotive industry, but in all industrial sectors, and capacity utilization continues to fall, with the situation recently getting noticeably worse. According to economic surveys by ifo, order backlogs in the construction and manufacturing industries are declining substantially, without new orders promising a revival. As private households are unsettled by the weak economic situation and are reluctant to spend, the strong rise in real wages and the associated increase in purchasing power are not (yet) being felt by manufacturers of consumer goods.

Negative Sentiment but Declining Inflation Gives Reason for Hope

According to the ifo Business Climate Index, the mood among German companies has deteriorated for the fourth time in a row due to the stagnation of the overall economy. The index fell from 86.6 points in August to 85.4 points in September. With the renewed downturn in sentiment, the all-important strengthening of economic performance is moving further into the future.

Nevertheless, falling inflation rates in Germany, just as in the rest of Europe, offer hope for an economic upturn. In September, inflation dropped below the 2% mark to 1.6% (July: 2.3%). This means that inflation in Germany is at its lowest level since February 2021. And as in the EU, energy is the main dampening factor, offset by disproportionately high price increases for services.

Wage increases and falling inflation rates mean that, on average, households have more money to spend. If confidence in economic development increases, positive macroeconomic stimuli are possible.

Development in the Road Freight Market

In the second quarter of 2024, the logistics indicator of the German logistics association BVL recorded not only an improvement in the business situation and business climate in road freight transport compared to the beginning of the year, but also higher business expectations. But following this upturn, the business climate in the German logistics industry weakened again in the third quarter. The BVL logistics indicator fell by 0.9 points to 84.4 points. In line with the overall economic development, logistics service providers again assessed both their current business situation and their business expectations as worse than in the previous quarter. They do not expect their business situation to improve over the next six months either. This is mainly due to the continuing decline in demand.

Despite this decline, the ratio of freight to cargo space in the EU was still higher in July (73:27) and August (71:29) than in 2023 (64:36 and 57:43 respectively), according to the TIMOCOM Transport Barometer. A seasonal increase in freight volumes is expected from September onwards due to the upcoming Christmas period. At 81:19, the current forecast for September 2024 is even higher than the figures for 2022 (78:22) and 2023 (66:34).

European Carriers Challenged by Driver Shortage

The driver shortage is also contributing to existing capacity bottlenecks. 48% of European transport companies expect to have great difficulty recruiting drivers in 2025. And in Germany alone, there was a shortage of about 70,000 truck drivers by 2023, with the trend increasing.

Another factor that drives bottlenecks is the rise in insolvencies, particularly in the transportation industry. In the first half of 2024, the number of insolvencies in Germany rose by almost 30% across all sectors. The logistics sector is generally considered to be particularly vulnerable to insolvency due to its low profit margins. In the UK, for example, twice as many transport companies filed for bankruptcy in 2023 as in the previous year, and in Germany, there were 9.1 insolvencies per 10,000 companies in the freight forwarding business in early 2024.

In addition to increasing economic pressures, transport companies are facing major challenges to survive in the market: decarbonization, digitization, demographic shifts and driver shortages, energy prices, and changing supply chains. To respond to these challenges, companies must adapt their structures and processes. This will take time and further investment.

Despite Falling Diesel Prices, Transport Prices Remain High

Prices for transportation are little changed from the previous quarter and remain at a high level in the third quarter of 2024. Even falling diesel prices cannot change the generally high freight rates. At the end of September, the weighted average price of diesel in the 27 EU member states was €1.51, which is a moderate level and compares with €1.79 at the end of September 2023. However, in contrast to the falling diesel price, labor costs, for example, increased by 4.7% in the second quarter of 2024. In addition, as of July 1, 2024, vehicles with a gross vehicle weight of 3.5 tons are subject to tolls in Germany. These developments, combined with rising costs for vehicle maintenance, insurance, and the necessary investments by transport companies in digitization and sustainability, are resulting in rising transport prices.

The Market Situation in Summary

Although inflationary pressures are steadily decreasing, the economic situation, especially in Germany, is stagnating with low or even negative growth. The relevant indicators show a subdued mood among German and European companies, both in terms of the general business climate and among logistics companies in particular.

Signs of a gradual recovery are cautious and mainly based on a possible increase in demand due to lower inflation and higher real wages. Whether this will help the economy to gain momentum is yet to be seen.

Outlook for Further Development

Against the backdrop of ongoing uncertainties regarding financial and geopolitical developments, an economic recovery in Europe, and particularly in Germany, is not expected by the end of the year. In the future, however, economic growth should increasingly be driven by rising household incomes, a robust labor market, and stronger foreign demand, while financing conditions will improve thanks to interest rate cuts.

This economic outlook implies that transport volumes are likely to increase again in early 2025, while freight rates are expected to remain at high levels.

The next update, which will be published in early January 2025, will highlight the market events of the fourth quarter of 2024 and the resulting impact on the road freight market. This will ensure continued open and transparent communication, which is a top priority for DHL Freight.