Commentary on the current situation in the European logistics industry and the load factor during the first quarter 2018 from Martin Veen, Head of M&A & Strategic Projects, DHL Freight. The macroeconomic conditions for European road freight transport are still favorable. The growth forecast of the European GDP has been corrected upwards from two to 2.4 percent. However, the overall sentiment is a bit more cautious, not the least because of the unstable conditions of global politics and a slight decline of certain indicators, such as the German business climate index. This in particular took a small hit at the end of the first quarter and currently resides at 2017 average levels. Likewise, the European Purchasing Managers Index (PMI) by HIS Markit shed a little value, but at 56.6 still resides on a high level and implicates a further rise in production output.

Industry specific factors

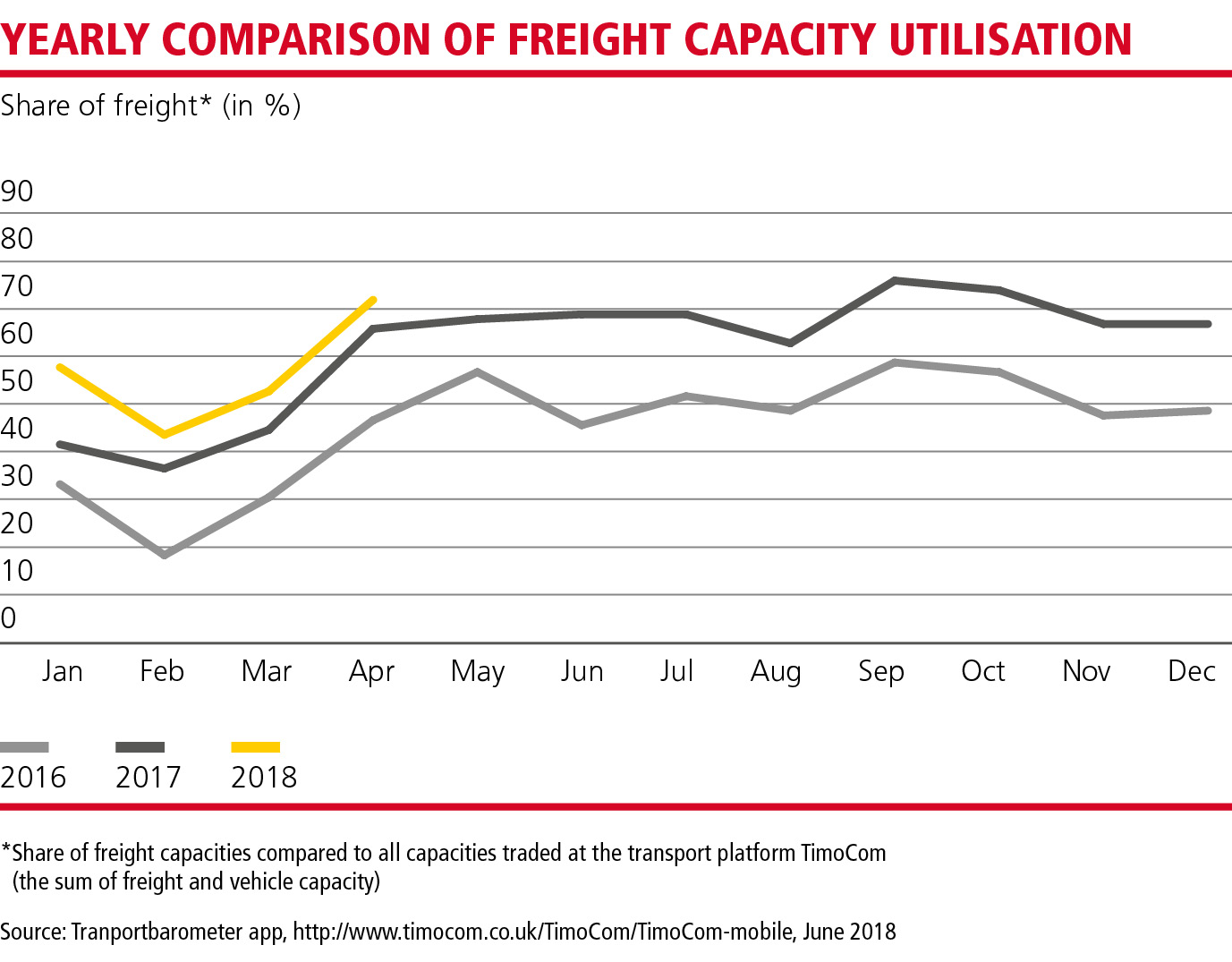

After shippers had more capacities at their disposal at the beginning of the year than at the end of 2017, this trend got reversed already in March. In contrast, Transporeons Transport Market Radar fixed the Transport Pricing Index at a value of 6.9 points above the comparative value of the first quarter 2017. This is an indicator that the market is still lacking enough cargo space and that this factor is gradually getting worse. This perception is supported by TimoComs figures for their European Transport Barometer, which calculated a ratio between demand and supply of 74:26. This shortfall is last but not least caused by a blatant shortage of qualified personnel throughout the industry, especially a lack of drivers. Consequential, rising wages are conceivable which, combined with the comparatively higher diesel prices to 2017, will push the overall costs in the transport industry further upward. In the long run these factors could put a dent in the economic growth alltogether. First indications for a lower capacity utilization due to supply chain constraints are visible.

Outlook

Despite a seasonally induced decline at the year’s beginning, freight volumes in road freight traffic are still firmly on a high level. Both in the field of Terminal Based Operations (TBO) and in Non Terminal Based Operations (NTBO), gains have been registered in comparison to the respective timeframe of last year. According to the European Road Freight Forwarding Index of Danske Bank, this will last a while. The index forecasts a continuously rising demand for transport. On the political side of things, the longest formation phase for a government in German history has come to a close. Albeit, the adjustments of political priorities as regards to road freight transport will last well into the summer months. In view of this fact, the influence of further political decisions on the overall market are impossible to prescind.

Shall we explore this topic in more depth?

Curious? Our authors will be happy to help you. Just send us a short message—and we'll dive deeper together.