Diesel prices comment by Eugen Weinberg, Head of Commodity Analysis at Commerzbank

Eugen Weinberg [Photo: Commerzbank]

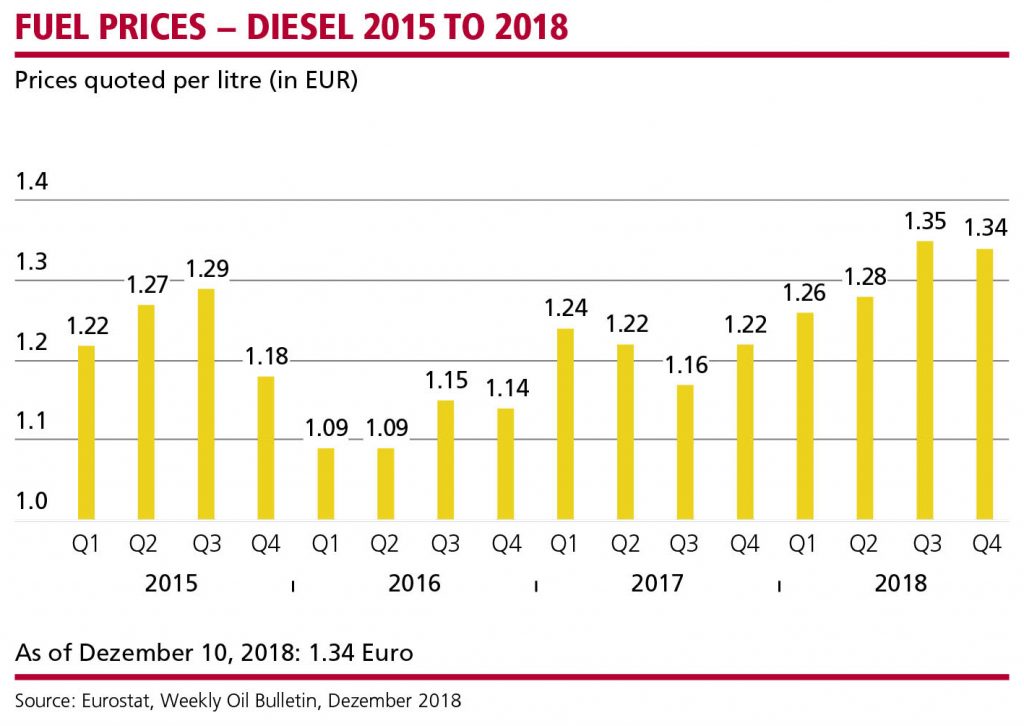

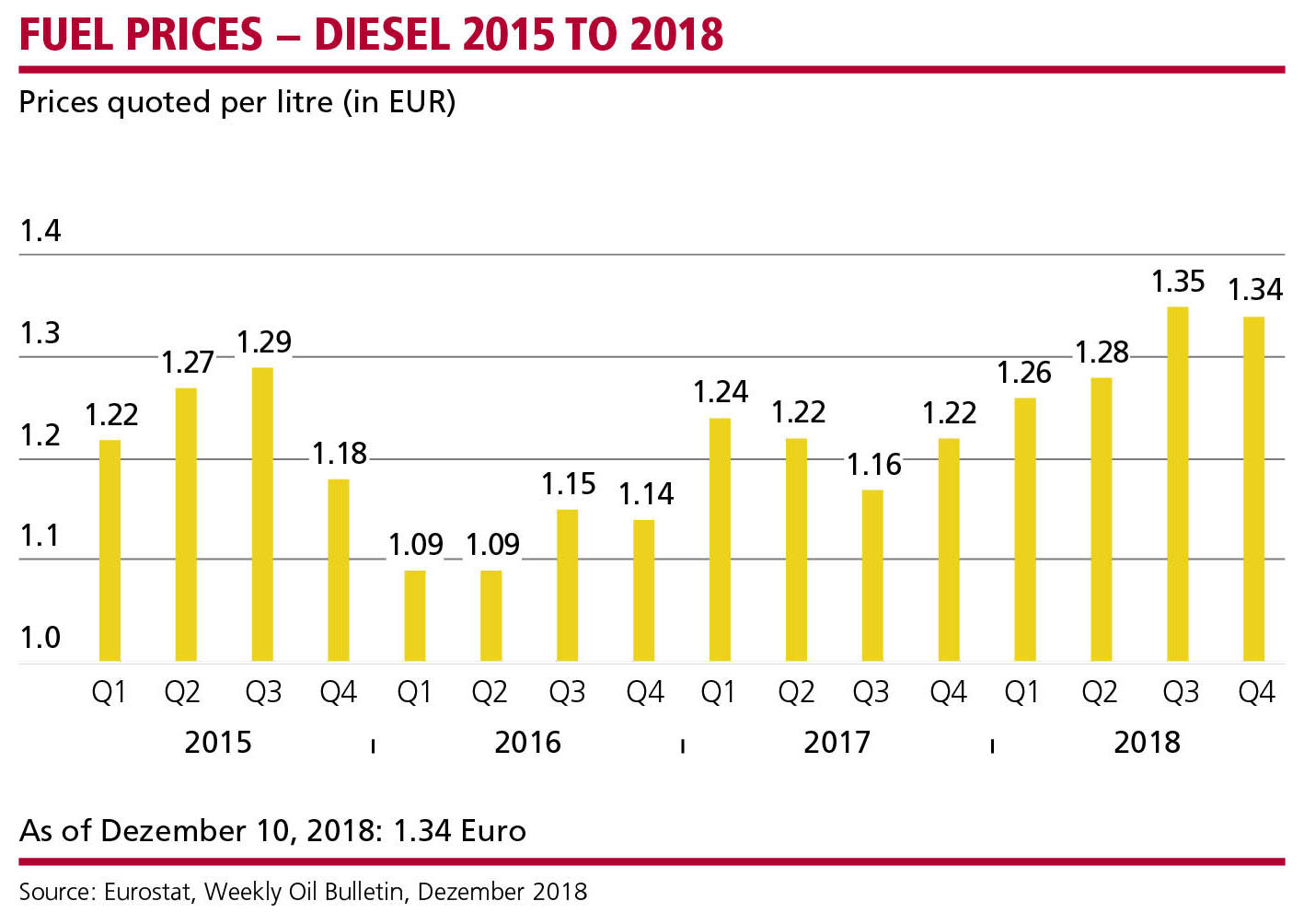

While the wholesale price for diesel fuel ranged at nearly 750 US-Dollar, respectively 650 Euro, per ton in October, it dropped to 550 US-Dollar or 480 Euro by the end of November. But this alleviation was never felt by a major part of the consumers, especially in western and southern Germany.

Low water levels entail higher prices

The reason for that was neither the autumn leave period nor possible collaboration between suppliers, but the water level of the Rhine recording an all-time low. Thusly, the water gauge was constantly below critical readings between October and November (30 cm and below at Emmerich, 180 cm at Duisburg-Ruhrort or 80 cm at Kaub). That massively impeded the fuel transport from Rotterdam. Long lasting low water periods are of great concern for inland waterway transport, as falling water gauges mean less load capacity for the barges. The incurred transport costs did rise accordingly, a development which was imparted upon the end user.

Rising prices ahead

The slump in prices did not went by the oil producers without their noting. Most of the leading crude oil exporters in conjunction with the OPEC agreed upon production cuts of 1.2 million barrels per day. To the total surprise of all, the Canadian province Alberta is also prepared to reduce its oil production by 325,000 barrels per day at the beginning of 2019. These steps should lead to the vanishing of the current surplus supply during the next six months. This is as the current demand has nothing to do with the price drop of crude oil. To the contrary, China for example did import more than ten million barrels per day a short while ago, more than ever before. Therefore, the oil prices should recover again in a short while, and could ascend to 70 US-Doller per barrel during the course of 2019.

Increase to more than 70 Dollars is possible

Certainly, there are scenarios in which the oil price could rise even higher. Firstly, it is entirly conceivable for the OPEC reducing its production more than agreed upon, to precipitate the recovery of prices. Also, the exemptions for Iranian oil exports expire at the beginning of May. A prolongation by the US government is doubtful. Also, it is not predictable if the dry period in Europe will replicate itself. The danger of a local shortage of supplies remains real, though. What's more, the IMO 2020 set of rules could cause the diesel market to run short in the medium term. According to this, as of January 2020 all ships have to use fuel with a maximum sulphur content of 0.5 percent instead of the 3.5 percent as yet. Due to these circumstances we are of the opinion that strategic measures against rising diesel prices are worthwhile at the moment. It does not matter if this is done by additional storage capacities, long-term purchase agreements with suppliers of financial safeguards.

Shall we explore this topic in more depth?

Curious? Our authors will be happy to help you. Just send us a short message—and we'll dive deeper together.