A restrained economic autumn left Europe facing major challenges in the fourth quarter of 2023 and the new year is not expected to bring any noticeable upturn. In this issue of DHL Road Freight Market News, we take a closer look at important details and trends of the months of October, November, and December 2023. Where does the EU economy stand after the fourth quarter of 2023 and how is European road freight transport developing? For information on the trends in the third quarter, please refer to our previous issue.

Geopolitical Tensions Shape the Global Economic Picture – European Implications and Outlook

The intensification of geopolitical tensions affected the global economy in the fourth quarter of 2023. Although GDP growth initially was stronger than expected, it diminished due to weak trade growth and tighter financial conditions, according to the OECD. For the year 2023 as a whole, the international organization predicts global economic growth of 2.9%, but this will slow to 2.7% in 2024. Given that inflation continues to fall and real incomes will rise, the forecast for 2025 is more promising at 3%. However, the reluctant optimism could become overcast sooner or later. The International Monetary Fund (IMF) recently warned that the division into the power blocs of the USA and European countries in the West and China and Russia in the East could contribute to the suffering of the future global economy.

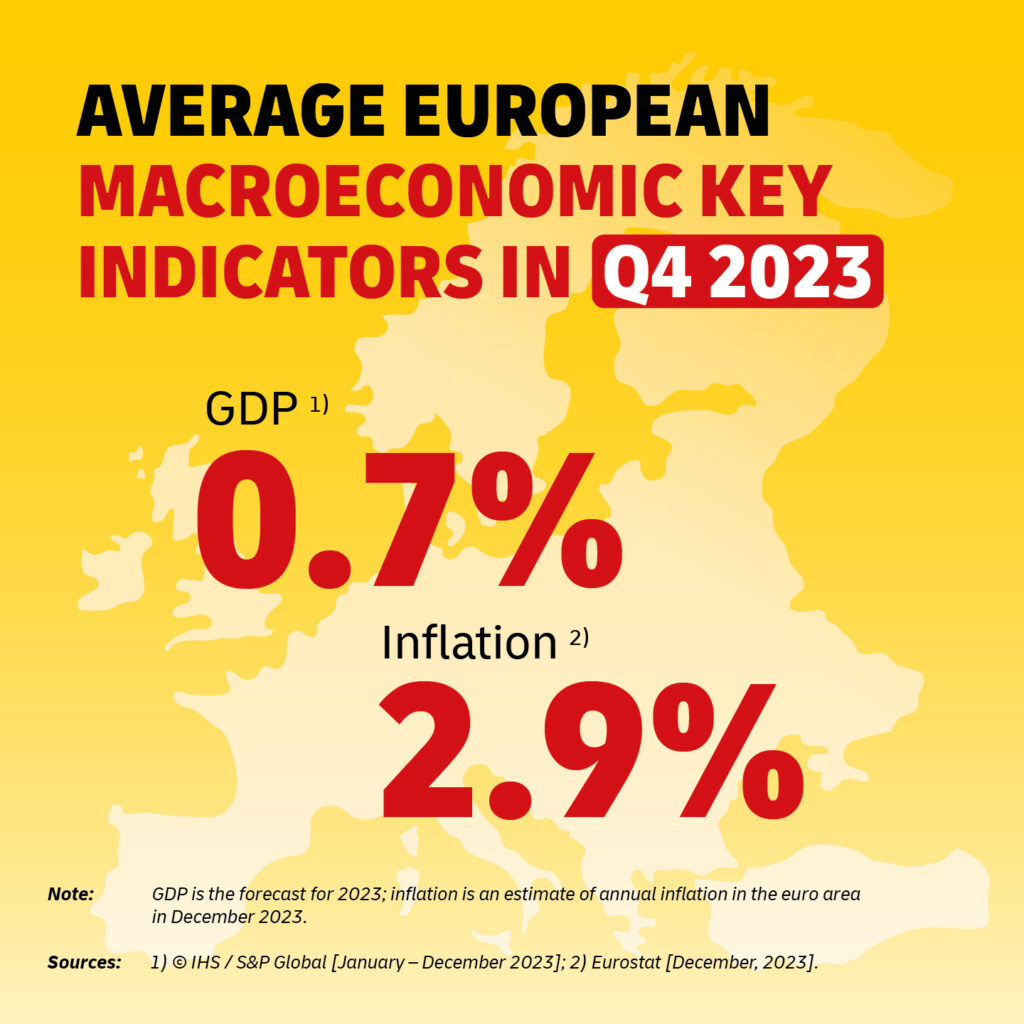

Europe is not spared from the global economic situation. After robust expansion in 2022, real GDP contracted towards the end of the year, after hardly any growth in the first three quarters of 2023. The still high, albeit declining, inflation and tighter monetary policy, in addition to weak demand, took a greater toll than anticipated. This was also the case in the fourth quarter, which additionally witnessed subdued economic activity. The European Commission recently estimated GDP growth of 0.6% in the eurozone for 2023, which is 0.2 percentage points below its summer forecast. S&P Global reports an only slightly more optimistic figure of 0.7%.

That said, the European Commission’s outlook on the year ahead is a little bit better. Economic activity in the EU is expected to gradually improve as consumption recovers thanks to a still robust labor market, sustained wage growth, and a further slowdown in inflation. Some subindices of the PMI (Purchasing Managers’ Index) also indicate that the lowest point may have been reached: the declines in incoming orders and purchasing volumes have abated. Overall, the companies surveyed expect business to improve. GDP growth in the EU is thus anticipated to increase to 1.3% in 2024. By contrast, the ECB and OECD outlooks are somewhat more subdued, with growth of just 1% and 0.9% respectively. While these figures are higher than those for 2023, the outlook and expectations remain cautious.

Germany in Economic Downturn – Forecasts for 2024 Revised Further Downwards

Germany is performing below other European countries. Although an official calculation of economic growth in 2023 will only be available in a few weeks’ time, economists and economic researchers have already made initial prognoses.

DIW Berlin, for instance, assumes an economic downturn of 0.3%, reflecting the general expectations, which all predict a decline in real GDP and thus anticipate a recession. This development can be attributed, among other things, to lower private consumption in recent months – contrary to initial expectations. The GfK and the Nuremberg Institute for Market Decisions consider the buying propensity better than before and even estimate that the consumer climate will recover moderately in January at -25.1 points compared to the summer of last year. Nevertheless, the consumer climate remains at a low level. The continuing uncertainty, coupled with a persistently high price level and incomes not rising at the same rate, offer little scope for a stronger recovery.

Sluggish investment activity and reduced foreign demand recently also had a negative impact on economic growth in Germany. Since the outbreak of the coronavirus pandemic, German foreign trade has only been growing due to rising prices, states the Kiel Institute for the World Economy (IfW). Sentiment among companies has also deteriorated. The ifo Business Climate Index fell to 86.4 points in December, down from 87.2 points in November. Against this backdrop, the companies surveyed are also sceptical about the first half of 2024.

Hopes that the lowest point has been reached by the fall of 2023 and that the new year could start with fresh impetus are fading more and more. Correspondingly, the predictions for 2024 have been revised downwards several times over the course of the past year and currently show an immense range. While especially banks tend to take a more pessimistic view of the coming year and anticipate a renewed contraction of the economic output, leading research institutes are expressing cautious optimism, even if some of their rather confident forecasts have been revised downwards in the meantime.

For example, the ifo Institute lowered its forecast for German economic growth in 2024 by 0.5 percentage points, but still expects positive economic output of over 0.9%. The DIW Berlin, on the other hand, is somewhat more pessimistic in its assessment. It has halved its original prediction and now only forecasts real GDP growth of 0.6% for 2024. This revision, as well as the general tentativeness in Germany, can also be associated with the loss of public funds. This comes as a result of a judgement by the German Federal Constitutional Court concerning the German “Fund for energy supply and climate protection”. This court decision significantly restricts the fiscal scope of the German government coalition.

Inflation in the Eurozone Drops Quarter-on-Quarter, then Increases Again in December

While annual inflation in the eurozone was still estimated at 4.3% in September, the inflation rate was predicted to fall in the months of the fourth quarter, reaching a level of over 2.4% in November, for example. In December, however, Eurostat announced a new rise in inflation and assessed annual inflation in the eurozone at 2.9%, driven by the factors “food, alcohol and tobacco” and “services”.

A similar trend is emerging in Germany: after the inflation rate had declined continuously until November, it rose again in December and is currently estimated at 3.7%. The annual average inflation rate in Germany is expected to be 5.9% for 2023, which is considerably higher than in the eurozone in general. It was consumer prices in particular that caused this increase and could further fuel the inflationary trend. According to the ifo Institute, a growing number of companies intend to raise their prices in the coming months. Furthermore, the rise in energy prices will probably extend into the first half of 2024, which additionally militates against an easing of the general price level.

Development in the Road Freight Market

The economic development in 2023 impacted all players in the road freight market, which were confronted with a continuous decline in volumes. The capacity situation improved significantly corresponding to this development, even though the ratio of freight to available cargo space remains imbalanced, albeit at a level that can be considered normal.

Following a shortage of capacity in the European road freight market in September, this trend continued in the fourth quarter. With a ratio of freight to available cargo space of 68 to 32, the figure in October remained at the previous month’s level, while in November there was a slight easing of the capacity situation (63 to 37). However, the availability of capacity decreased again in December due to rising demand for transport services in the run-up to Christmas. The TIMOCOM transport barometer recorded a ratio of freight to cargo space of 66 to 34.

In contrast to year-end 2022, when there was an increase in available capacity, the development of the freight-to-capacity ratio in the European road freight market returned to a typical seasonal pattern at the end of 2023.

Diesel Prices Have Fallen Slightly – Freight Rates Remain Consistently High

The development of the diesel price in 2023 resembles a sine curve: after falling prices in the first half of the year, the cost of diesel fuel has risen continuously since June and peaked in September (€1.79). Since then, diesel prices again have declined continuously. In October, the weighted average for the 27 EU member states was still €1.75 per liter, in November it was only €1.69. By December, the price of diesel had returned to the July level (€1.64). At the moment, it is hard to predict how the price of diesel will evolve, especially in view of the ongoing geopolitical tensions.

That said, the current diesel price situation is still not evident in freight rates, which are still at a high level. This applies to both contract rates and spot rates. The latter increased noticeably, especially in December, which results from the seasonality outlined above. Freight rates are unlikely to fall in the future either. On top of generally rising costs, for instance because of wage adjustments, players in the road freight market have a responsibility to invest in climate-friendly solutions for the sector. In addition, truck tolls are being raised or adjusted in many European countries. After new toll rates came into force in Germany in December, further increases will follow this year in Austria and Lithuania, for example.

The Market Situation in Summary

Leading research institutes and banks are pessimistic about Europe’s economic situation. After a weak economic year 2023, no substantial upturn is expected this year either. Wars in Europe and the Middle East as well as ongoing financial uncertainty among consumers are having a negative impact on the general willingness to invest and offer little scope for economic recovery.

The flagging market situation has a corresponding effect on the European road freight market. While volumes are expected to develop only moderately, capacities are at a comparable level to the years before the pandemic. As such, they are on a course towards normalization. Despite this and falling diesel prices, freight rates are still at a high level, not least because of rising toll rates (still pending in some European countries).

Outlook for Further Development

Considering the current economic trends in conjunction with ongoing geopolitical tensions, a positive turnaround in the economic situation is unlikely in the short to medium term. For the time being, the economic situation will continue to be unsatisfactory in 2024 and thus have a corresponding impact on the road freight market, which must expect a further decline in demand – at least in the first half of 2024.

The next update, to be published in early April 2024, will focus on the economic events of the first quarter of 2024 and the resulting impact on the road freight market. This will ensure continuous open and transparent communication, which is a top priority for DHL Freight.